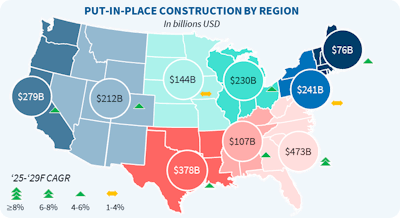

The U.S. construction industry is nearing the trough of its current cycle, with early indicators pointing to a gradual rebound beginning in 2026, particularly in nonresidential and infrastructure segments that are concrete-intensive. Ducker Carlisle forecasts that total put-in-place construction will rise by 5.3 percent and grow at an average annual rate of 5.7 percent through 2029. However, consensus forecasts from organizations such as the American Institute of Architects (AIA) and the National Association of Home Builders (NAHB) project more moderate growth of 1–3 percent.

These conservative expectations reflect a challenging macroeconomic environment characterized by elevated long-term interest rates, declining consumer confidence, rising tariffs, and persistent labor shortages. Nonetheless, recent actions by the Federal Reserve and expectations of further rate cuts have renewed optimism among market participants that improved funding conditions will stimulate broader construction activity in the coming years.

Residential Construction

Following two years of higher borrowing costs and subdued demand, the U.S. residential construction market is stabilizing after a prolonged downturn. Our outlook indicates that the sector is positioning itself for measured growth through 2029, even as regional trends remain uneven.

As interest rates begin to ease, the housing market is expected to stabilize in 2025 and rebound into 2026 as builders work through existing backlogs and prepare for additional rate cuts to spur single-family home starts. The majority of new housing activity remains concentrated in the South, suggesting that concrete contractors serving these markets can expect rising demand for concrete materials, slab foundations, and masonry block or brick installations.

For concrete contractors, this points to improving bid volumes tied to foundations, flatwork, and masonry in high-growth Southern markets.

Concrete Solutions & the Data Center Expansion

Among the most dynamic areas of construction is the surge in data center development. These projects have become one of the fastest-growing drivers of nonresidential construction, as well-capitalized technology and cloud-service companies continue to invest heavily in expanding capacity. This momentum is driven by ongoing demand for cloud storage, video streaming, and, increasingly, artificial intelligence (AI) and data analytics infrastructure.

We estimate that data center construction will surpass $50 billion by 2029. While large-scale greenfield projects dominate industry headlines, there is also a growing trend toward retrofitting and repurposing existing facilities, particularly those located near established power and energy grids. This trend creates substantial opportunities for concrete contractors, as these facilities require extensive structural reinforcement, poured foundations, tilt-up wall systems, and enhanced energy and water management infrastructure.

For concrete contractors, data centers represent higher-spec work with stricter tolerances, heavier reinforcement, and longer project timelines, rewarding firms that can execute consistently at scale.

Additionally, ancillary developments such as office and high-occupancy support facilities are expected to benefit from this expansion. In contrast, traditional commercial office construction remains constrained by soft occupancy and declining rental rates. Notably, data centers are expected to be a significant source of future electricity demand, with consumption projected to more than double by 2028.

Manufacturing Renaissance

Although manufacturing construction typically moderates following a period of strong expansion, recent shifts in U.S. trade and industrial policy over the past several years are driving renewed domestic investment. Tariff adjustments and incentive programs have encouraged global corporations and sovereign wealth funds to commit significant capital toward U.S. manufacturing projects. This influx of investment is expected to sustain medium-term growth in construction activity, technological innovation, and facility modernization across the sector.

Regional Dynamics

The Southern United States is projected to continue outperforming other regions, accounting for nearly half of total national construction spending by 2029. This sustained growth is supported by structural trends such as net inbound migration, relatively affordable housing markets, and ongoing post-disaster reconstruction efforts.

High-growth states include Texas, Georgia, Arizona, Utah, the Carolinas, and Colorado. Within these regions, suburban and rural markets, particularly Tier-2 and Tier-3 cities are expected to capture outsized development as builders seek lower-cost land and streamlined permitting environments.

These regions are also among the most concrete-intensive markets, driven by population growth, logistics facilities, manufacturing plants, and infrastructure rebuilds.

Emerging Trends for Concrete Contractors

Despite favorable demand conditions, evolving industry dynamics present new opportunities for concrete contractors to enhance competitiveness and long-term performance:

Consolidation: Ongoing challenges related to succession planning, workforce shortages, and geographic diversification are accelerating consolidation among contractors. Strategic mergers and acquisitions, often supported by private equity or outside investors are expected to accelerate through the decade, helping balance market influence between contractors and increasingly consolidated suppliers and distributors.

Distribution Partnerships: While some contractors have recently adopted limited inventory-holding strategies for high-volume products, the variability of project requirements and specialty materials continues to favor strong distributor partnerships. Collaborative relationships with distributors can improve supply-chain efficiency and reduce working-capital strain, ensuring contractors maintain flexibility while mitigating risk.

How six rapidly deployable AI solutions—from automated quoting and intelligent data search to AI-driven proposals, lead generation, financial automation and admin support—are transforming efficiency and profitability across the walls and ceilings industry

By: Fabien Cros

Tighter margins, rising material costs and an array of other factors are creating mounting pressure on the walls and ceilings industry to optimize operations to stay competitive.

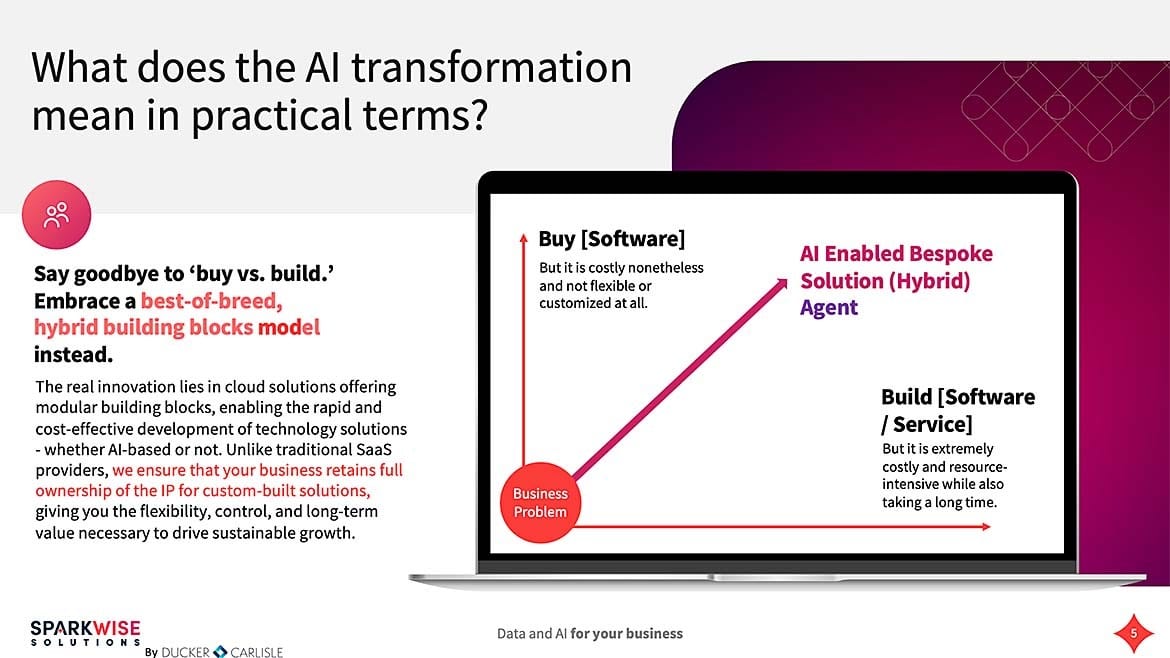

Artificial intelligence can be a powerful ally in meeting this challenge, but adoption has been hindered by two major obstacles: first, uncertainty about where to begin to achieve the most immediate and impactful results; and second, the fact that most AI deployments have required costly and time-consuming custom development.

Newer solutions are solving both problems by providing pre-built applications specifically designed to deliver tangible benefits. From automating routine back-office tasks to improving lead generation, here are six rapidly deployable applications that enable contractors, interior specialists, architects and suppliers to work more efficiently and in ways that are already demonstrating significant bottom-line returns for early adopters.

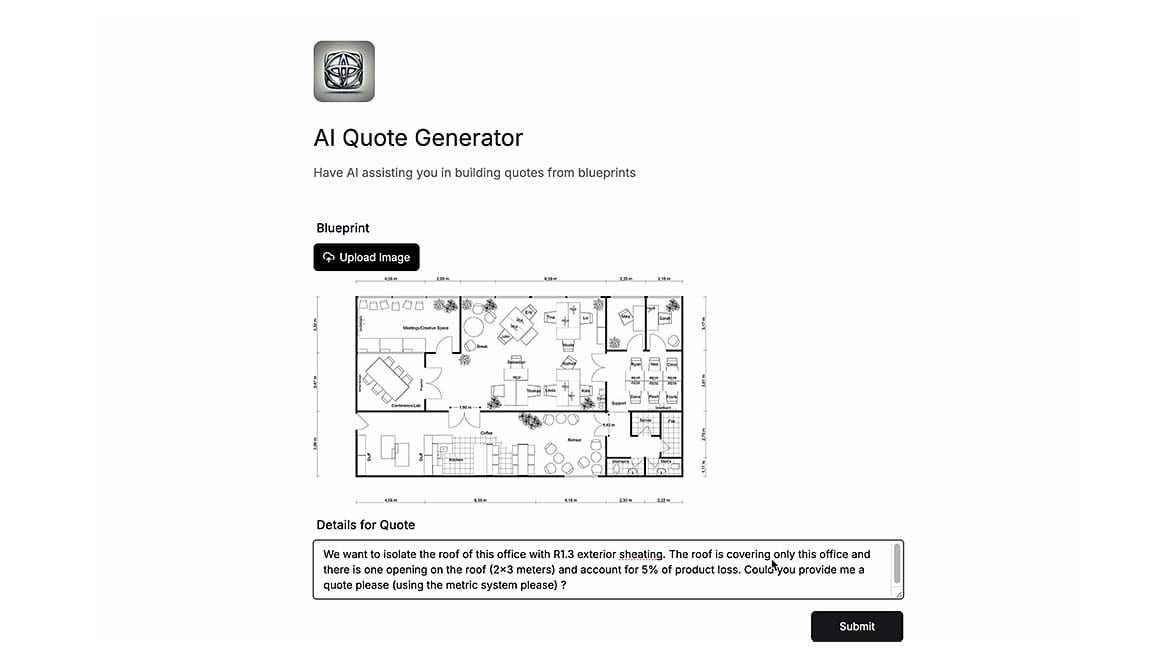

1. The Quoting AI Agent: Precise Bids in Minutes, Not Days

Creating an accurate and competitive bid has traditionally required hours of poring over architectural drawings, detailing square footage for drywall, calculating linear feet for trim, estimating materials for stucco, or specifying acoustic panel layouts.

AI-powered Quoting Agents can now automate the process of reading blueprints and specifications to quickly identify and quantify every element—from the number of gypsum boards and their fastening points to the precise application area for EIFS or the specific type and amount of insulation required. By ingesting vast amounts of project data and learning from your past successful bids, these solutions can rapidly analyze new plans, generating highly accurate cost estimations for materials, labor, and even factoring in waste.

This accelerates your bid process, enhances accuracy, and frees your skilled estimators to focus on strategic project analysis and client relationships, ultimately boosting your win rate.

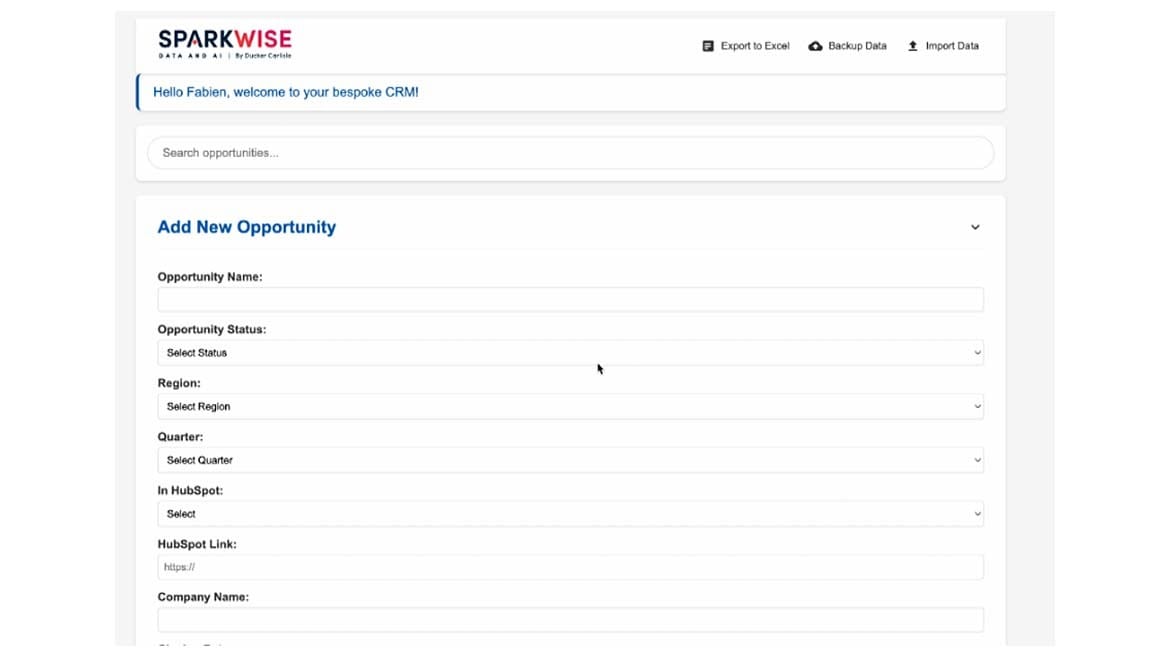

2. Intelligent Data Management: Your Project Legacy, Instantly Accessible

Every wall and ceiling project generates an enormous volume of valuable data, including past proposals, material specifications, acoustic reports, submittals, change orders, punch lists and supplier agreements. This information is typically scattered among multiple IT systems, project managers’ laptops or even physical archives. Hours can be wasted trying to locate the specific fire-rated drywall specifications from a project five years ago when needed for current projects.

AI-driven data management centralizes and intelligently organizes all your historical project data. Advanced AI search capabilities then enable you to query the system, “Find all projects using Type X gypsum board and a specific EIFS system in the last two years” and retrieve the exact documents and details in seconds. This empowers faster, more informed decision-making, streamlines material procurement, and ensures you never waste time hunting for information you already possess.

3. The Bid & RFP AI Agent: Winning Proposals Powered by Data

Winning a bid often comes down to who can submit the most compelling, detailed and insightful proposal. Manually gathering all the necessary information – from accessing a multitude of public bid portals to researching a client’s specific needs, analyzing a project’s neighborhood, or understanding a building’s history – is a time-consuming and often incomplete process. The result is a generic proposal that may not stand out from the crowd.

This is where the Bid & RFP AI Agent provides a game-changing advantage. This AI can access and monitor all available bids, including the vast landscape of public RFPs. It also automatically collects and analyzes thousands of additional data points about a potential project such as the neighborhood’s demographics, the building’s historical use, or the surrounding market conditions. It then produces an intelligent, data-driven proposal in as little as five minutes, leveraging its analysis to inform the best strategy, recommend competitive pricing, propose a realistic timeline, and even suggest specific materials or solutions aligning with the client’s unique needs. This level of insight ensures your proposals are not just submissions but compelling, highly customized arguments for why you are the best firm for the job.

4. Harnessing AI for Next-Generation Lead Generation: Be Found Where It Matters

The traditional landscape of lead generation, heavily reliant on SEO and website optimization, is evolving rapidly. A powerful new channel for client acquisition is emerging, driven by the increasing use of conversational AI platforms like ChatGPT and similar AI assistants. Homeowners, general contractors and architects are increasingly turning to these AI tools to ask questions, such as “Who are the best acoustic ceiling installers in this region?” or “Which stucco contractors have experience with intricate architectural details?”

While the entire industry will eventually adapt, early movers who optimize their presence and articulate their expertise within these new AI ecosystems will gain a substantial competitive edge. AI can help you understand the nuances of natural language queries, identify client intent, and craft compelling narratives that position your firm as the authoritative expert. By proactively integrating AI into your marketing strategy today, you can capture new leads from a rapidly growing segment and outmaneuver competitors still relying on yesterday’s tactics.

5. Automating Accounts Payable and Receivable: Precision & Savings

Efficient invoicing, payment processing and robust cash flow management are critical for the financial health of your business, but Accounts Payable and Accounts Receivable often remain manual, error-prone and time-consuming tasks. From processing material invoices for insulation to generating payment requests for finished drywall installation, these transactional duties consume valuable administrative time.

AI-powered solutions for AP/AR are exceptionally adept at these precise, repetitive functions. They can automatically extract and verify data from supplier invoices, cross-reference against purchase orders, flag discrepancies for human review, schedule payments, and even dispatch automated reminders for outstanding client invoices. This reduces human error, helps accelerate payment cycles, improves cash flow, and yields significant administrative cost savings. It also enables your human finance team to focus more on strategic financial planning, analysis, and actively supporting your business development efforts.

6. AI for Administrative Automation: Liberating Your Team for Craftsmanship

The administrative overhead in wall and ceiling firms is considerable, often diverting skilled team members from their core competencies. While previous automation tools offered some relief, their rigid rule-based nature often fell short of the needs of a busy contracting business.

The advent of Large Language Models and advanced AI can dramatically lessen the load. Imagine AI bots autonomously generating CRM inputs after a job site visit, drafting routine safety updates for the crew, checking inventory levels for specific drywall types or EIFS components, or sending personalized reminders to clients about acoustic panel delivery or to suppliers about metal stud shipments. Assigning these “boring stuff” tasks to AI can save countless hours while also empowering your project managers, estimators and administrative staff to focus on complex problem-solving, quality control, client engagement, and the craftsmanship that defines your trade.

While the initial foray into AI might seem a grand undertaking, beginning with these six pre-built use cases not only gets you up and running quickly and affordably but also ensures that you will realize a significant return on your investment. Eliminating paperwork bottlenecks and improving lead generation can help you work smarter—and that’s always good for the bottom line.

Supply chains run on data as much as they do on trucks, containers, and warehouse space. Every movement generates information, from supplier forecasts to shipping manifests, yet most organizations struggle to make sense of it fast enough to act. Artificial intelligence (AI) is now changing that reality, helping manufacturers, distributors, and logistics networks move from reacting to anticipating.

While the technology is proven, the challenge for many companies lies in understanding where AI can make the biggest, most immediate difference. Here’s how practical applications are already improving speed, accuracy, and margins across industrial, automotive, and manufacturing operations.

The AI librarian: Turning data chaos into clarity

In most supply chains, valuable data lives in silos; ERP systems, email threads, spreadsheets, and even paper archives. The result is operational blind spots that slow decision-making. For instance, an automotive supplier might lose hours verifying whether a shipment of brake components is complete or partial, delaying production.

An AI librarian addresses this by creating a centralized intelligence hub that can read and organize every document across the business. Using natural language processing, it extracts, classifies, and connects unstructured data from invoices to inspection reports into one accessible knowledge base. A warehouse manager can simply ask, “Show me the bill of lading for order #10342,” and the system retrieves it instantly, regardless of where it was stored.

In one industrial case, a manufacturer reduced administrative search time by 70%, freeing teams to focus on managing vendors and logistics instead of chasing documents. The result isn’t just efficiency; it’s transparency, a single version of truth for the entire operation.

Automating accounts payable and receivable

For many businesses, accounts payable (AP) and accounts receivable (AR) are still dominated by manual reconciliation. Teams match purchase orders, invoices, and receipts line by line, often under tight deadlines. Errors in these processes can ripple through the supply chain, delaying shipments, straining supplier relationships, and distorting cash flow forecasts.

AI-powered automation can now manage these workflows end-to-end. It reads invoice data, validates it against purchase orders, flags discrepancies, and even schedules payments or reminders. In one automotive aftermarket supplier, AI automation reduced invoice processing time from five days to less than one, while improving accuracy by 40%. Another global manufacturer used AI to reconcile payments across 12 ERP systems, cutting manual effort by half and improving on-time payments to key suppliers.

This kind of automation doesn’t replace finance teams, it elevates them. Freed from repetitive data entry, teams can focus on analysis, planning, and strategic supplier management.

Intelligent process automation: Raising the floor for routine work

Administrative load remains one of the biggest drains on supply chain efficiency. Robotic process automation (RPA) made early progress here, but traditional rule-based bots couldn’t handle nuance. With today’s AI and large language models (LLMs), automation can now interpret context, adapt to new scenarios, and interact more naturally with people and systems.

Consider a logistics firm that uses AI agents to draft purchase orders after sales meetings, monitor inventory across multiple sites, or alert planners when delivery delays threaten production schedules. In the automotive sector, AI bots now track hundreds of supplier shipments simultaneously and notify production managers when parts risk arriving late. Industrial equipment companies are using similar systems to review maintenance logs, identify machines nearing service thresholds, and automatically schedule technician visits.

These capabilities don’t remove people from the process, they give them better leverage. Employees spend less time transcribing and checking, and more time problem-solving, negotiating, and improving processes. In one example, a European electronics manufacturer used AI-driven process automation to reduce administrative workload by 30% while improving order accuracy across its supplier network.

The path forward

AI’s value in supply chain management is not theoretical, it’s already measurable. The most successful companies aren’t trying to automate everything at once; they’re starting with targeted use cases that deliver clear ROI and scale from there.

Practical, pre-built AI solutions like data retrieval systems, financial workflow automation, and intelligent process orchestration can be implemented in weeks, not years. Each adds resilience, speed, and insight to a part of the business that has historically been slow to change.

The next evolution of supply chain leadership won’t hinge on who moves the most goods, but on who best turns information into action.

Traditionally, automobiles contain hundreds of structural metal parts that people never see. Whether it’s full front or rear underbodies, shock-tower modules or floor structures, they act as the “skeleton” of cars and trucks. Multiple components are riveted and welded together to form a safe, reliable framework and is covered with body panels.

However, automakers such as Ford, General Motors, Honda, Hyundai, Rivian, Tesla, Toyota and Volvo are rethinking that process. They are investing in new technology that enables them to produce large castings.

Tier One suppliers, such as Aisin and Ryobi, are also bullish on gigacasting. The goal is to consolidate parts, reduce complexity and eliminate weight.

A Big Idea

Gigacasting—also referred to as hypercasting, megacasting and unicasting—uses high-pressure aluminum die-casting to produce very large, single-piece structural components. It appeals to automotive engineers who are struggling to address the unique lightweighting challenges posed by electric vehicles.

Several companies make gigacasting equipment, including Bühler, IDRA and LK Machinery.

“Megacasting is an evolutionary step in die-casting,” says Michael Cinelli, head of product management and marketing at Bühler Group. “It uses the same fundamental physics, but applied at a dramatically larger scale, and with higher structural and quality requirements.

“It leverages ultra-large die-casting machines that generate between 6,000 and 9,000 tons of locking force,” explains Cinelli. “Megacasting relies on optimized alloys, advanced thermal management and integrated process control.”

Looking for quick answers on assembly and manufacturing topics?Try Ask ASM, our new smart AI search tool.Ask ASM→

Bühler unveiled its first ultra-large press in 2020 as automakers around the world began demanding more efficient production processes to meet the requirements of next-generation vehicles. Since then, the company has sold more than 50 Carat series machines to a variety of OEMs and suppliers.

Designed specifically for gigacasting applications, the huge presses feature die locking forces up to 92,000 kilonewtons. For instance, the Carat 920 machine can inject more than 200 kilograms of liquid aluminum into a die within milliseconds.

“This approach simplifies manufacturing, reduces vehicle weight and improves structural performance,” claims Cinelli. “With fewer joining processes and less material waste, megacasting also supports more sustainable production. It is suitable for both traditional and electric vehicle architectures.”

Gigacasting (right) reduces assembly complexity. Illustration courtesy Tesla Inc.

According to Cinelli, gigacasting’s rise reflects a convergence of trends in the auto industry, such as maturing technology, market pressure and a more capable supply ecosystem. “The barriers were significant for years, and only recently have they been cleared, largely within the past five,” he points out.

“In short, megacasting required simultaneous progress in presses, tooling, alloys, simulation, and a compelling economic and architectural driver,” says Cinelli. “Those pieces only aligned recently, triggered by EV-focused manufacturing strategies and proven early implementations, enabling rapid adoption after decades of technical interest.”

“Several factors have only recently converged to make gigacasting feasible at scale,” adds Leonard Ling, senior analyst and automotive knowledge manager at Ducker Carlisle Worldwide LLC. “The introduction of ultra-large presses, combined with advances in high-strength, heat-treat-free aluminum alloys, now allows for large, dimensionally stable castings.

“EV architectures offer more flexibility in underbody design and benefit significantly from reduced weight and simplified assembly,” notes Ling. “In contrast, traditional ICE platforms and legacy tooling investments made such large integrated castings uneconomical in the past.

“Gigacasting delivers meaningful structural and cost advantages,” claims Ling. “It can dramatically reduce part counts, welds and assembly operations, while improving dimensional accuracy. Fewer joints and more uniform load paths enhance stiffness and crash performance.

“For EV manufacturers, simplification means faster platform development, lower capital intensity and weight savings that translate directly into extended range,” says Ling. “The process also supports local manufacturing, as large castings are often produced adjacent to final assembly plants, cutting logistics costs and emissions.”

New Production Philosophy

In North America, Tesla has been the only high-volume adopter of large, high-pressure die-casting, using it on the Model 3, Model Y and Cybertruck.

“Ford and GM are moving in that direction and have sourced giga-press equipment, but remain in early deployment phases,” explains Ling. “European automakers are more cautious. Volvo is the clear front-runner, investing heavily in megacast rear floors for its next-generation EVs, while most German OEMs are still running pilots.

“Asian automakers, particularly in China, are advancing the fastest,” Ling points out. “BYD, Geely/Zeekr, Li, NIO and XPeng, among others, already use gigacast front or rear modules and battery housings in production, with some experimenting with casting nearly the entire underbody.”

Megacasting disrupts decades of a “we always do it this way” mindset in the auto industry.

“For legacy automakers, integrating gigacasting into existing plants remains a hurdle, requiring reconfiguration of body shops and balancing new investment with existing stamping capacity,” says Ling. “Beyond the press itself, gigacasting depends on a complete casting ecosystem. That includes large melting and holding furnaces, vacuum systems to control porosity and tight temperature management throughout the process.

“Heavy automation handles ladling, part extraction and trimming, along with localized heat treatment or quenching where needed,” explains Ling. “Quality assurance is equally critical. High-end X-ray or CT scanners, ultrasonic inspection, dimensional measurement cells and straightening systems are all required to monitor and correct defects or distortion in these massive structural parts.”

While it is technically feasible to convert traditional automotive body shops to gigacasting, it’s far from a plug-and-play process.

“A conventional body shop built around hundreds of stamped panels and weld points must be re-engineered to accommodate a handful of very large castings instead,” says Ling. “That means new fixtures, updated joining methods, such as bonding or hybrid welding, and reconfigured conveyors and handling systems for heavier parts.

“Complete revalidation of crash and corrosion performance is also necessary,” notes Ling. “In addition, repair networks need retraining.

“In practice, OEMs can adapt portions of an existing body shop, but full integration of gigacasting usually aligns better with a new EV platform or major retooling effort rather than a retrofit,” warns Ling.

Automakers and suppliers are investing in high-pressure machines that enable them to mass-produce large castings. Photo courtesy Bühler Group

Parts Consolidation

One of the biggest advantages of gigacasting is its ability to consolidate parts and eliminate time-consuming assembly processes. That enables engineers to replace complex stampings with single, cast structures by combining geometry, functions and interfaces.

“Engineers can integrate multiple sheet metal stampings into one net-shape component,” says Bühler’s Cinelli. “Cast-in ribs, bosses and flanges replicate stiffness and joining features previously created by separate brackets and reinforcements. Overlapping panels, hem flanges and spot-weld seams can be eliminated by using continuous wall sections and local thickening.”

Functional features that previously needed add-on parts can be embedded, such as:

Mounting points—cast threaded bosses or machined pads for suspension, seats, batteries, crash rails and power train mounts.

Joining features—lap/plug-weld zones, adhesive channels and self-piercing rivet landings, reducing separate reinforcements.

Cable and pipe management—cast clips, channels and through-holes for wiring harnesses, brake lines and coolant lines.

NVH features—stiffening beads, rib lattices and tuned thickness transitions can be used instead of separate braces.

In addition, engineers can consolidate crash structures and load paths. Design ribs, crush initiators and energy-management features can be integrated directly into castings to replace multiple boxed sections and add-on crash brackets. Shock towers, subframe attachments and load transfer nodes can be combined into a single underbody and front or rear module.

Subassemblies can be reduced through interface integration. Floor pans, crossmembers, rocker reinforcements, and rear rails can be combined into one casting, minimizing fixture sets and welding sequences. With cast-in datum features for body alignment, fewer locator brackets and machining fixtures are needed.

According to Cinelli, engineers can leverage localized thickness and tailor topology. “Variable wall thicknesses, gussets and lattice ribs can be used to place material only where needed—replacing stacked stampings used for stiffness,” he points out.

“Conformal cooling and precise filling allow thin walls in low-load regions, avoiding extra patch panels,” adds Cinelli. “Fasteners and sealers can also be minimized, because continuous-cast walls remove many lap joints, reducing seam sealers and mastic pads.”

This sport utility vehicle made in China features gigacast subassemblies. Photo courtesy XPeng Inc.

Gigacasting Applications

Tesla Inc. pioneered automotive gigacasting several years ago. The automaker used the technology to produce front and rear underbodies on the Model Y sport utility vehicle, sharply cutting part counts and welds.

Tesla engineers adopted large megacastings to produce a three-piece chassis that consists of a structural battery pack sandwiched between front and rear castings. The massive components eliminated more than 350 stamped steel parts, including brackets. Megacasting also enabled Tesla to reduce the size of its body shop.

“The front casting includes the left and right shock towers, the wheel arch, the crush can for the front bumper, and the left and right door hinge pillars,” says Cory Steuben, director of cost engineering at Lucid Motors who previously participated in several tear downs of Tesla vehicles when he served as president of Munro & Associates. “The rear casting is even longer.

“Castings are like stones,” explains Steuben. “They provide amazing structural rigidity, because they don’t flex like many types of stamped steel subassemblies. They are attached to the rest of the vehicle with threaded fasteners and structural adhesives.”

Tesla engineers pioneered gigacasting technology. Photo courtesy Munro & Associates

Engineers at other automakers have also been intrigued by the potential of megacasting. They see it as a key enabler in the quest to produce a $25,000 EV for the mass-market.

Rivian Automotive Inc., for instance, has announced that its next-generation R2 platform will employ large structural castings for the underbody. In fact, by using the technology throughout the vehicle’s body structure, the automaker expects to eliminate 50 metal stampings and get rid of more than 300 joints.

Ford Motor Co. plans to use gigacasting as part of the Universal EV Production System that it’s in the process of installing at the retooled Louisville Assembly Plant. The technology will form the backbone of its Universal EV Platform, which will feature a structural battery pack sandwiched between a front and rear structure.

“Large single-piece aluminum unicastings [will] replace dozens of smaller parts, enabling the front and rear of the vehicle to be assembled separately,” says Jim Farley, president and CEO of Ford. Farley predicts the new process will reduce parts by 20 percent vs. a typical vehicle, with 25 percent fewer fasteners, 40 percent fewer workstations and 15 percent faster assembly time.

Honda Motor Co. engineers are also bullish on the potential of gigacasting. The automaker recently installed six Bühler Carat 610 presses at its engine plant in Anna, OH. The machines are producing two-part battery enclosures that will serve as the main frame structure for the floor of next-generation Honda and Acura EVs. The front and rear sections are joined together using friction stir welding.

In addition, Honda is conducting extensive research at its technical center in Tochigi, Japan. Engineers are experimenting with different casting conditions and parameters, such as temperature, pressure, speed and cooling rate.

Large front and rear castings may be used in more vehicles in the near future. Illustration courtesy XPeng Inc.

Numerous Challenges

Despite lots of hype and promise, gigacasting has several disadvantages over traditional automotive production processes. Some of the biggest hurdles, for instance, involve finding materials that can be formed and joined reliably.

Other challenges include keeping large thin-walled parts dimensionally stable, maintaining consistent casting quality and using tooling that holds up while still allowing quick changeovers.

“Casting has been around forever, but defects and stress concentrations are always a challenge,” warns Dilip Banerjee, Ph.D., a research engineer who specializes in mechanical performance at the Center for Automotive Lightweighting at the National Institute of Standards and Technology. “Die-cast parts must also be able to absorb the energy of impacts that can occur during vehicle crashes.”

Crashworthiness depends on smart designs. Specifically, how cast ribs, joining zones and alloys are engineered for ductility in as-cast form.

“Uniform cooling is critical, because during solidification the composition can change,” explains Banerjee. “Microstructures are prone to porosity caused by bubbles or voids, which can lead to ductility problems. High-quality, pore-free castings are essential to avoid thermal destruction.”

“Gigacasting brings new challenges in equipment cost, die durability, quality control and repairability,” adds Ducker Carlisle’s Ling. “Machines above 6,000 tons require significant infrastructure investment and extremely precise process control to avoid porosity, distortion or cracking.

“Tooling and dies are expensive, each costing several million dollars and requiring frequent maintenance,” says Ling. “That means that gigacasting is more economical for high-volume vehicle programs where costs can be amortized across large production runs.”

Gigacasting presses enable automotive engineers to consolidate parts, reduce complexity and eliminate weight. Photo courtesy Bühler Group

Ling believes that broader adoption in the auto industry will depend on continued progress in several areas, including:

– Capital investment. “Giga presses, auxiliary systems and facility modifications represent multimillion-dollar commitments, still a barrier for many automakers and Tier One suppliers,” says Ling..

– Material development. “Current alloys often carry licensing costs and patent limits,” explains Ling. “Many OEMs are developing proprietary alloys that balance strength and ductility without post-casting heat treatment.”

– Production flexibility. “Gigacasting equipment is specialized for a limited number of large parts, which can constrain flexibility across multiple vehicle platforms,” notes Ling.

– Process reliability. “Improving die-life management, dimensional control and nondestructive inspection remains key to consistent mass production,” Ling points out.

– Sustainability. “While gigacasting minimizes material waste, it is energy-intensive, warns Ling. “Closed-loop recycling systems for complex aluminum alloys will be essential to making the process truly sustainable.”

– Market dynamics. “If EV growth slows or shifts geographically, OEMs may hesitate to commit to capital-intensive infrastructure,” says Ling.

“For legacy automakers, integrating gigacasting into existing plants remains a hurdle, requiring reconfiguration of body shops and balancing new investment with existing stamping capacity,” concludes Ling.

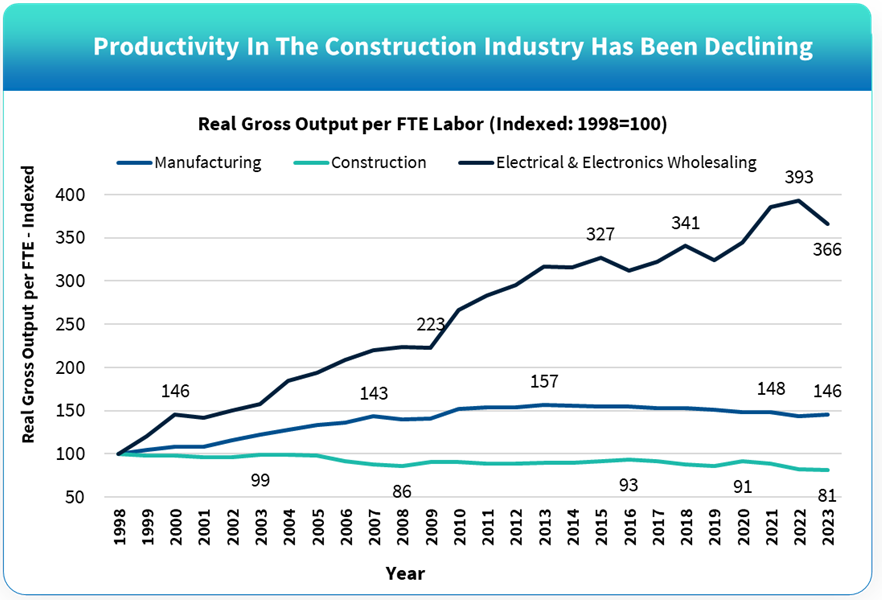

Labor productivity growth in the U.S. has slowed sharply since 2010, and in manufacturing it has declined outright. Construction productivity has been sliding for decades. For companies that serve these sectors, this is both a warning sign and a growth opportunity. The players that help customers work faster, smarter and with fewer errors will win market share, command premium pricing and build stickier relationships.

Why This Matters Now

Productivity in manufacturing and construction is not a theoretical problem. It shows up as:

Margin pressure on every project

Delays from rework, RFIs and coordination gaps

Talent stretched thin across complex jobs

Difficulty defending price against low-cost competitors

Your customers feel this every day. The partners who help them claw back productivity will win the next decade.

What You’ll Learn in the Paper

The white paper, Solving the Productivity Problem: A Blueprint for Growth in Manufacturing and Construction, breaks down:

What is really driving the productivity slowdown in manufacturing and construction

How labor, technology, and process issues combine to erode performance

A four-step approach to turn customer productivity gaps into commercial advantage

A real case study of a supplier that repositioned as a productivity partner and saw measurable impact

Practical questions and prompts to uncover new value for your own customers

Who Should Download This

Leaders in industrial, manufacturing and construction focused businesses

Commercial, sales and marketing teams selling into these sectors

Strategy and product owners shaping value propositions and offerings

Private equity investors backing industrial and construction platforms

Turn Productivity Pressure Into Growth

Productivity pressure is not going away. The question is whether you respond as a commodity supplier or a productivity partner. Use this paper to sharpen your strategy and give your teams a clearer story on how you help customers do more with less.

Download the Whitepaper Get the full 14-page report with data, frameworks, and a real-world case study you can put in front of your leadership team tomorrow.

Kerry Smith possesses more than 30 years of published writing experience in construction, architecture, engineering, commercial real estate, IT, economic development and more. Prior to acquiring CNR as its new owner in November 2023, Kerry served as CNR’s editor for six years. She founded the Illinois Business Journal in 2000. For samples of Kerry’s writing, see https://www.informationworks.org/blog-1.

Chris Fisher of Ducker Carlisle outlines how smart positioning and specialization will define winners

To begin, could you share details of your career history and how you came to be in your current position?

I’ve spent over 30 years in the global construction and industrial sectors, working both in consulting and on the operating side in corporate development for multinational corporations. Today, I lead Ducker Carlisle’s Global Building and Construction practice, where we help corporate executives and private equity firms grow, improve, and advance their businesses.

After two years of tightening conditions, your latest outlook suggests the US construction market is finding its floor. What signals are you seeing that indicate the downturn is nearing its end?

The most important signal is the Federal Reserve’s decision to cut its benchmark rate and signal the potential for further reductions in 2026. Combined with improving economic conditions, this will lift sentiment among builders and consumers. We’re also seeing steady investment and project planning in data centers and reindustrialized light manufacturing tied to Al growth and domestic trade policy. In addition, commercial occupancy levels and business cashflows are improving; two reliable indicators of future investment.

You forecast a housing rebound by early to mid-2026. What factors will drive that recovery, and how quickly do you expect builders to regain momentum once interest rates begin to ease?

There’s pent-up demand among both move-up and first-time buyers waiting for mortgage rates to drop below six percent. Historically, it takes two or more quarters for rate cuts to translate into lower mortgage rates that stick. We anticipate further reductions ahead, which should drive renewed momentum in housing later in 2026. Southern states are expected to capture nearly half of all national construction spending by 2029.

What’s behind this regional strength, and how should contractors and suppliers be positioning themselves to take advantage?

The South continues to lead due to strong population growth, housing demand, and employment levels. Developers are drawn by available land, business-friendly tax policies, and a longer construction season. The best way to grow is to follow growth, contractors should be rebalancing geographic capabilities and positioning themselves where demand is strongest.

Nonresidential construction is showing resilience, particularly in data centers, healthcare, and lodging. What distinguishes these sectors from others in terms of growth potential and investment appeal?

Each sector has unique demand drivers. Data centers are fueled by Al and the race among tech firms to expand processing capacity at scale. Healthcare construction remains strong given its share of national GDP and the need for diverse facility types, from hospitals to outpatient centers. Lodging, while cyclical, is benefitting from rising consumer spending on travel and experiences, particularly among younger, experience-driven demographics.

Data center construction alone is projected to exceed $50 billion by 2029. How is this surge reshaping demand for materials, labor, and project delivery models?

Data centers have highly specialized requirements; structural, thermal, and electrical that not every contractor can meet. We’re seeing firms create dedicated teams focused solely on data center projects, following investor demand nationwide. This specialization has tightened labor availability and extended lead times for traditional projects, opening new opportunities for contractors serving adjacent sectors.

Labor shortages and cost inflation continue to pressure margins. How are contractors leveraging Al-driven bidding, off-site manufacturing, and other innovations to stay competitive?

Leading contractors are using Al to identify and bid on the right projects faster, manage labor allocation, and improve conversion rates. Many are also investing in off-site manufacturing and modular assembly to improve predictability and reduce labor intensity. Were seeing more collaboration and partnership models across project types and regions, as firms experiment with outsourcing and self-perform strategies. in trades like electrical, HVAC, and building envelope, some contractors are capturing more value through prefabrication, bundled services, and light fabrication.

When it comes to supply chain efficiency, what trends are you seeing around value-add distribution, and how might this change relationships between manufacturers, distributors, and contractors?

The professional contractor channel is being reshaped by well-capitalized players like Home Depot, Lowe’s, and OXO, who are using technology and scale to drive productivity and simplify procurement. At the same time, tariffs have shifted sourcing dynamics, creating opportunities for domestic manufacturers and distributors to take on more of the acquisition, assembly, and supply functions traditionally handled overseas.

As the market transitions from contraction to gradual growth, what risks should construction leaders keep top of mind?

Construction leaders should focus on disciplined execution and service quality, resisting the urge to overextend in pursuit of short-term gains, Growth without process and people readiness can undermine long-term performance, Clients have long memories, and firms that consistently deliver quality, meet deadlines, and communicate effectively are the ones that secure repeat business.

How is investor sentiment evolving around the construction and building products sector, and what does that mean for M&A activity or capital investment over the next few years?

Investor interest is strong. Private equity is now focused on contractor service platforms after years of consolidation in distribution. The sector benefits from multiple growth drivers-underbuilt housing, reindustrialization, and long-term infrastructure spending. These fundamentals make construction one of the more attractive segments for capital investment over the next cycle.

Looking toward 2029, what defines success for the construction firms that emerge strongest from this cycle

Like past cycles, we typically see the high performers have invested and optimized their business to build advantage or strong competencies which include:

– Sticky customer relationships and strong customer value propositions

– Consistent execution and quality of offering or experience – reliability and consistency are key

– Demonstrated capabilities to form partnerships and innovate across investment, design, supply and installation.

– A business doesn’t have to own or control all aspects to form valuable, committed partnerships

– Al and technology enabled execution will be particularly important

– Ability to pursue and adjust business mix across regions, project types, product segments and value chains.

Agility and collaboration will define the next generation of construction leaders.

French executives from PSA were numerous in Carlos Tavares’ inner circle. Since Antonio Filosa took the helm, former Fiat Chrysler executives have been setting the pace.

See Original Version In French

See Original Version In French

Les dirigeants français issus de PSA étaient nombreux au sein de la garde rapprochée de Carlos Tavares. Depuis l’arrivée d’Antonio Filosa aux commandes, les ex-Fiat Chrysler donnent le tempo.

Où sont passés les «frenchies» de Stellantis ? Au fil des remaniements du comité exécutif du groupe, désormais piloté par Antonio Filosa, « vétéran » de feu l’américano-italien Fiat Chrysler, les ex-PSA sont devenus des spécimens rares. Le casting de l’équipe de management a d’abord été revu en février, puis en juin, en octobre et même en novembre pour la région Europe élargie. Plusieurs figures de l’équipe de Carlos Tavares, maintenues dans un premier temps par John Elkann lorsqu’il était directeur général (DG) intérimaire, ont depuis été effacées de la photo de famille. Exit Maxime Picat, le patron des achats, Yves Bonnefont, celui de la division logicielle, Brigitte Courtehoux, la chef des nouvelles mobilités, Olivier Bourges en charge de l’expérience client, Arnaud Deboeuf, le patron des opérations industrielles… Seuls quelques-uns ont été épargnés comme Grégoire Olivier, responsable de la région Chine et Asie Pacifique, Sébastien Jacquet, en charge de la qualité, ou même le DRH, Xavier Chéreau, toujours aux manettes.

Moins de six mois après l’arrivée du nouveau DG, la « leadership team Stellantis » est désormais dominée par des ex-Fiat Chrysler : sur les quatorze membres de ce comité exécutif, huit sont issus de Fiat Chrysler, quatre de PSA et deux sont des outsiders. Sous l’ère du précédent patron Carlos Tavares, les anciens de PSA étaient à l’inverse en supériorité numérique. En janvier 2021, sur les 43 dirigeants de Stellantis, 25 venaient de PSA. Ce qui suscitait la critique des équipes américaines et italiennes : l’état-major du dirigeant portugais était décrit comme une armada de « Yesmen » – des béni-oui-oui. Assiste-t-on aujourd’hui à un retour de balancier au profit de Fiat Chrysler et d’Exor, le holding familial des Agnelli (15,9% du capital) ?

L’ancrage français ne semble plus peser lourd alors que la famille Peugeot représente encore 7,9% du capital de Stellantis, et que Bpifrance en possède 6,6%. Les fidèles de Filosa sont désormais basés comme lui aux États-Unis, sauf si leur poste est directement rattaché à une autre région. 13 milliards de dollars d’investissements aux États-Unis (sur cinq ans) ont été annoncés par le nouveau patron il y a quelques semaines, créant la stupeur en France et en Europe. Quant au siège européen d’Amsterdam, il a perdu de sa pertinence : le cœur européen de Stellantis est à Turin en Italie, fief des Agnelli.

Stellantis aimanté par les États-Unis et l’Italie

À part les membres de la famille Peugeot, cette évolution ne choque plus personne sur le terrain en France. La culture de la performance de PSA et la fierté d’avoir appartenu à cette branche, paraissent s’être dissoutes dans la fusion. Filosa et son entourage semblent avoir conquis les cadres : « 30% des VP et SVP – vice-présidents et senior vice-présidents – sont français, alors que la France ne représente que 15% des effectifs », assure l’un d’eux, relayant les données communiquées dans l’Hexagone par la direction de Stellantis pour mettre les pendules à l’heure. Il n’y a aucune chasse aux Français. Beaucoup étaient arrivés à l’époque de Carlos Tavares et sont partis après son départ », observe cet ancien de PSA. Qui trouve normal que le nouveau boss s’entoure de personnes qu’il connaît et en qui il a confiance.

Même oreille bienveillante chez les syndicats. «J’avais interpellé le DRH sur le déséquilibre de la gouvernance au détriment de la France dans un courrier, souligne Laurent Oechsel, délégué syndical central CFE CGC. Lorsqu’il est venu dans l’Hexagone le 3 novembre dernier, Antonio Filosa nous a rassurés sur l’importance de notre pays pour l’ensemble du groupe. Les origines des dirigeants nommés n’ont plus autant d’importance aujourd’hui. Nous sommes un groupe mondial en pleine transformation. Il est nécessaire de faire travailler tout le monde ensemble sans chercher à savoir d’où on vient. »

Les syndicats relèvent aussi que le dialogue social est plus ouvert. «Filosa est beaucoup plus à l’écoute», remarque le représentant de la CFE CGC. «Ceux qui sont restés apprécient que les pouvoirs soient de nouveaux délégués. Le système est devenu plus sain», remarque Bertrand Rakoto, consultant automobile aux États-Unis chez Ducker Carlisle.

Le «charme« Filosa fonctionne en interne

Comment les nouveaux dirigeants de Stellantis ont-ils réussi à convertir les équipes tricolores ? Leur recette pourrait être résumée en un mot : régionalisation. Désormais, le management de Stellantis est organisé en grandes régions mondiales, chacune pilotant ses marques, son design, ses objectifs financiers. Un héritage de la gouvernance en vigueur à l’époque de Fiat Chrysler. L’Europe élargie est désormais l’horizon des marques françaises et italiennes et des salariés, chacun étant maître chez soi. Un changement radical par rapport à l’organisation pyramidale privilégiée par Tavares, où toutes les décisions remontaient à lui et à son entourage.

D’abord choisi pour diriger cette grande zone, le Français Jean-Philippe Imparato a finalement été remplacé par un Italien, Emmanuele Cappellano, entré chez Fiat Chrysler en 2002. Mais Peugeot, Citroën et DS sont chacune supervisée par des Français bien décidés à redynamiser leurs marques en faisant vibrer la corde locale. En parallèle, plusieurs cadres français ont été promus à l’échelle européenne, dont Christophe Montavon, l’ex-directeur de l’usine historique de Sochaux qui vient de prendre la responsabilité de l’ensemble des usines européennes.

Chaque région pilote ses marques

Le charisme d’Antonio Filosa a aussi joué pour embarquer les Français dans l’aventure. Le patron a su trouver les mots et le ton. À Poissy, où un «green campus» (centre de R&D et bureaux) flambant neuf jouxte l’usine, l’Italien est monté sur la scène de l’amphithéâtre, le 3 novembre, pour s’adresser aux cadres supérieurs en compagnie de Gilles Vidal, le célèbre designer français qui a fait la gloire récente de Renault avec les R5, R4 et nouvelle Twingo électrique, avant de revenir «à la maison ». «Nous avons tous ressenti une belle énergie, raconte un participant. Nous n’avions pas éprouvé ça depuis longtemps.» Le lendemain rebelote. Cette fois, Filosa était accompagné des patrons des marques françaises Peugeot, Citroën, DS, pour une intervention retransmise en direct auprès de l’ensemble des salariés. Le nouveau patron de Stellantis a rappelé que 2 milliards d’euros ont été investis cette année en France, tant dans les usines que dans la R&D, et que l’an prochain, 1400 embauches étaient aussi prévues.

En revanche, l’Italien n’a pas évoqué le plan de départs volontaires mené en parallèle en France. Ni les scénarios envisagés à moyen et long terme pour l’Europe. Or, d’après les informations divulguées lundi par le Financial Times, qui aurait eu accès à des présentations internes, Stellantis aurait prévu d’abaisser sa production de 11% en France entre 2025 et 2028. «Tout le monde reste sur sa faim, en attendant le plan stratégique prévu mi 2026, reconnaît Bertrand Rakoto, de Ducker Carlisle. Mais cette prudence se justifie, vu le contexte. Les décisions européennes seront bientôt prises sur les normes d’émissions de CO2 en Europe. En Amérique du Nord, les accords commerciaux entre le Mexique, le Canada et les États-Unis sont en renégociation. Cette prudence tranche avec les déclarations provocatrices et à l’emporte-pièce de l’ancien dirigeant du groupe.» Quel que soit le contenu du plan stratégique, en Europe, les dirigeants ont compris que leur budget à l’ébauche dépendrait du niveau de cash qu’ils seront capables de dégager. «L’année 2026 ne sera pas faste, mais 2027 devrait permettre de générer des ressources supplémentaires», témoigne l’un d’eux.

Aujourd’hui, une bataille s’est engagée au sein de la famille Peugeot, pour désigner le représentant de la dynastie au conseil d’administration de Stellantis. Un des candidats milite en faveur d’une présence plus forte de la famille au capital. La désignation devrait avoir lieu avant la fin de l’année, pour une soumission à l’assemblée générale en 2026. Mais cela ne renversera sans doute pas la suprématie des Agnelli.

Where have all the French executives of Stellantis gone? With each reshuffle of the group’s executive committee, now led by Antonio Filosa, a veteran of the defunct Italian-American Fiat Chrysler, former PSA executives have become a rare breed. The management team was first reshuffled in February, then again in June, October, and even November for the broader European region. Several figures from Carlos Tavares’ team, initially retained by John Elkann when he was interim CEO, have since been removed from the picture. Out go Maxime Picat, the head of purchasing; Yves Bonnefont, head of the software division; Brigitte Courtehoux, head of new mobility; Olivier Bourges, in charge of customer experience; Arnaud Deboeuf, head of industrial operations… Only a few have been spared, such as Grégoire Olivier, head of the China and Asia Pacific region; Sébastien Jacquet, in charge of quality; and even the HR director, Xavier Chéreau, who remains at the helm.

Less than six months after the arrival of the new CEO, the Stellantis leadership team is now dominated by former Fiat Chrysler employees: of the fourteen members of this executive committee, eight come from Fiat Chrysler, four from PSA, and two are outsiders. Under the previous CEO, Carlos Tavares, former PSA employees were, conversely, in the majority. In January 2021, of Stellantis’ 43 executives, 25 came from PSA. This drew criticism from the American and Italian teams: the Portuguese CEO’s staff was described as an army of “yesmen.” Are we now witnessing a swing of the pendulum in favor of Fiat Chrysler and Exor, the Agnelli family holding company (15.9% of the capital)?

The French connection no longer seems to carry much weight, given that the Peugeot family still represents 7.9% of Stellantis’s capital, and Bpifrance owns 6.6%. Filosa’s loyalists are now based in the United States, like him, unless their position is directly linked to another region. A few weeks ago, the new CEO announced $13 billion in investments in the United States (over five years), causing astonishment in France and Europe. As for the European headquarters in Amsterdam, it has lost its relevance: Stellantis’s European heart is in Turin, Italy, the Agnelli stronghold.

Stellantis Drawn to the United States and Italy

Apart from members of the Peugeot family, this development no longer shocks anyone on the ground in France. PSA’s performance-driven culture and the pride of having belonged to that division seem to have dissolved in the merger. Filosa and his entourage appear to have won over the executives: “30% of VPs and SVPs – vice presidents and senior vice presidents – are French, while France represents only 15% of the workforce,” asserts one of them, relaying data released in France by Stellantis management to set the record straight. “There’s no witch hunt against the French. Many arrived during Carlos Tavares’s time and left after he departed,” observes this former PSA employee, who finds it perfectly normal that the new boss surrounds himself with people he knows and trusts. The unions are equally receptive. “I had raised the issue of the governance imbalance, which was detrimental to France, with the HR Director in a letter,” emphasizes Laurent Oechsel, central union representative for the CFE-CGC. “When he came to France on November 3rd, Antonio Filosa reassured us about the importance of our country to the entire group. The origins of appointed executives are no longer as important today. We are a global group undergoing a major transformation. It is essential to get everyone working together without worrying about where they come from.” The unions also note that social dialogue is more open. “Filosa is much more attentive,” observes the CFE-CGC representative. “Those who stayed appreciate that the powers are now held by new representatives. The system has become healthier,” notes Bertrand Rakoto, an automotive consultant in the United States at Ducker Carlisle.

The Filosa “charm” works internally.

How did Stellantis’ new leaders manage to win over the French teams? Their recipe could be summed up in one word: regionalization. Stellantis’ management is now organized into large global regions, each managing its own brands, design, and financial objectives. This is a legacy of the governance in place during the Fiat Chrysler era. A broader Europe is now the horizon for the French and Italian brands and their employees, each with their own internal authority. A radical change compared to…

Sometimes, the fastest way to onboard AI software is through the back office.

Artificial intelligence holds real promise in helping the construction industry build smarter, more profitably and with greater operational precision, but the challenge for most firms is simple: Where to begin? Which AI tools will deliver the biggest operational and financial return? And how do we undertake AI initiatives without expensive custom development?

The answer is to embark on your AI journey by focusing on automating key back-office administrative and business development tasks. Off-the-shelf AI applications that can be tailored to your firm’s workflows can make that happen—taming repetitive paperwork, streamlining data collection and even strengthening your pipeline with smarter lead-generation tools—all without months of costly IT programming.

Here are six examples that can be implemented quickly and begin impacting the bottom line almost immediately after rollout:

1. The Quoting AI Agent: Accelerating Bids, Boosting Win Rates

The traditional quoting process is a labor-intensive exercise of interpreting blueprints, calculating materials and estimating labor hours. This not only consumes dozens of skilled hours but also limits the number of bids that a firm can realistically pursue and win. That’s where AI-powered quoting agents come in.

These systems can automatically read blueprints, identify specifications, quantify materials and generate precise cost estimations. By ingesting past project data and learning from a firm’s historical performance, they can produce highly accurate quotes in minutes—not days. This makes it possible to increase your bid volume, enhance bid accuracy and free up your most valuable estimators to focus on strategic pricing and client relationships. The resulting increase in your win rate and operational efficiency is a direct lift to your profitability.

2. Intelligent Data Management: Turning Scattered Data into a Strategic Asset

In any construction firm, proposals, contracts, project schedules, safety reports, supplier agreements and other data sources are typically scattered across various IT systems, individual laptops and physical files. This siloed information is a major liability, making it nearly impossible to quickly access and leverage your corporate knowledge base. The result is wasted time, duplicated effort and a lost competitive advantage.

AI-driven data management solves the problem by centralizing and intelligently organizing all your historical project data regardless of its original format and using advanced AI search capabilities to zero in on the information you’re looking for. Need to find a specific subcontractor’s safety record from a job five years ago or analyze material costs across all projects from the last quarter? You can now query your data and get precise answers in seconds, improving back-office productivity as well as enabling better forecasting, risk management and strategic decision-making.

3. The Bid and RFP AI Agent: Winning With Data-Driven Intelligence

Winning a large commercial or industrial contract hinges on far more than a good price; it requires a deep understanding of the project, the client and the market. Manually researching public bids, analyzing a project’s location and gathering competitive intelligence is a time-consuming and often incomplete process. Most firms rely on guesswork and limited information, leading to sub-optimal proposals.

A bid and RFP AI agent provides a powerful strategic advantage. It can access and monitor all available public and private bids, automatically collect thousands of additional data points about a potential project, and analyze the local market, building history and regulatory environment. This allows you to go from a generic, manually crafted proposal to a data-driven, pre-written proposal in under five minutes, complete with optimized pricing, a realistic timeline and even suggested project management approaches. These highly customized, compelling bids can significantly increase your chances of winning.

4. Harnessing AI for Next-Gen Lead Generation: Secure Your Competitive Advantage

The marketing landscape for construction is changing. While search engine optimization remains important, business leaders and procurement managers are increasingly turning to conversational AI platforms like ChatGPT to ask questions such as: Which firms have the best safety record for industrial projects in the Midwest? And: Who are the top contractors for institutional renovation?

Pre-built AI systems can help firms understand these natural language queries, identify a client’s true intent and automatically generate content that highlights the firm’s unique strengths, experience and value proposition. Moving quickly to integrate these tools into your marketing strategy can boost your visibility and associated business leads compared to competitors still relying on traditional SEO.

5. Automating Accounts Payable and Receivable: Optimizing Financial Performance

Accounts payable and accounts receivable processes are often manual, error-prone and a drain on resources. From processing hundreds of subcontractor invoices to ensuring timely payments from clients, these tasks can tie up a finance team in administrative work, preventing them from focusing on more strategic financial management.

AI-powered AP/AR solutions can automatically extract and verify data from invoices, cross-reference against purchase orders, flag discrepancies for review and send out automated payment reminders for outstanding accounts. That translates into reduced administrative overhead, minimized errors, optimized cash flow and a more robust financial operation. That in turn enables your financial team to focus on what truly drives profitability: forecasting, analysis and strategic financial planning.

6. AI for Administrative Automation: Unleashing Team Potential

The administrative burden in construction firms diverts valuable human capital from critical functions like project management and onsite safety. Previous automation tools like robotic process automation were often too rigid for the dynamic, real-world complexity of a construction business. With the advent of advanced AI and large language models, however, the scope for administrative automation has expanded dramatically.

AI bots can now handle non-core tasks such as automatically generating CRM entries after a site meeting, drafting routine safety updates, checking and updating inventory levels across multiple projects, and sending reminders to subcontractors about critical deadlines. This not only eliminates busywork but also enhances productivity across the entire organization, freeing your project managers, estimators and top administrative staff to focus on the high-value work that directly impacts productivity, quality and your company’s profitability.

Beginning with these six use-cases can help you unlock AI’s potential quickly, from trimming unnecessary overhead and freeing resources to focus on more productive tasks, to boosting business development efforts. Embracing these AI solutions now positions your business to stay ahead in today’s increasingly competitive construction industry.

The Recycled Materials Association (ReMA) recently updated its ISRI Specifications1 to approve the addition of a new scrap specification, called “vesper.” The new specification was developed in partnership with Novelis and other partners in the recycling supply chain. Vesper is designed to meet the growing demand for recycled wrought products (sheet, extrusion, and/or plate), which have stricter requirements regarding the amount of inclusions in the scrap stream.

Growing Demand for Recycled Wrought Products

Demand for aluminum is increasing across a variety of sectors from automotive to aerospace, packaging, and critical infrastructure. According to Ducker Carlisle, aluminum demand for the automotive sector will reach 556 lbs per vehicle by 2030—compared to 120 lbs per vehicle in 1980.2 In addition to increased demand, automotive and other industries are responding to growing interest in more sustainable products, requiring increased use of post-consumer scrap to lower the carbon footprint of the aluminum.

When automobiles reach end-of-life (EOL), they are disassembled and shredded, resulting in the production of zorba and twitch scrap grades. Zorba is a scrap mix sourced from the recycling of shredded EOL vehicles, electrical waste, and other goods, with an aluminum content of 70–90% combined with other metals. Twitch is generally produced from zorba, which has been sorted to contain 91–93% aluminum.

“Twitch typically contains a combination of cast and wrought aluminum recovered during the shredding of cars and EOL products,” said Gary Gallo, senior manager, recycling technology, Novelis. “Because of the high silicon content in the cast alloys, twitch is generally used by the secondary industry to make new cast products, like wheels, engine blocks, and transmission housings. Any wrought aluminum content in twitch has historically been downcycled away from its original form and repurposed into cast products. Once this happens, it can no longer be recycled into new sheets or extrusions due to high silicon levels.”

Ford introduced its all-aluminum F-150 in 2014 and has since used aluminum in its Navigator and Expedition models. As Gallo pointed out at the 2025 ReMA Convention & Exhibition, these Ford models and other aluminum-intensive vehicles are starting to reach the end of their life, leading to increased proportions of wrought alloy content being found in twitch (compared to cast alloys).3 It’s important to automakers and producers like Novelis to recover this wrought material instead of allowing it to be downcycled.

Therefore, the new vesper grade is specified to be made up of aluminum extrusion, sheet, and/or plate (wrought aluminum),1 which has been segregated from zorba or twitch. According to ReMA, the material must contain no more than a maximum of 1% free magnesium, 1% free zinc, and 0.5% free iron, as well as no more than 1% free non-metallics. In addition, the material must be dry and free of excessively oxidized material, air bag canisters, or any sealed or pressurized items.

“The vesper specification was created to draw attention to the market need for a new scrap stream explicitly focused on recycling the wrought fraction of twitch,” said Bea Landa, vice president of Metal Procurement and Recycling for Novelis North America. “It provides a precise definition of scrap content and represents a clear opportunity for the scrap industry to create value by sorting twitch into new, high-value specifications, which can be consumed into a wider variety of products.”

Gallo also pointed out that much of the twitch scrap stream is exported outside of North America due to insufficient domestic demand for cast products. “Processing this material into vesper creates new domestic markets that help to keep critical raw materials from leaving the country, while adding value for all participants,” he noted. “The production of vesper also helps to improve the circularity of sheet and extrusion products by recycling wrought scrap back to wrought products.”

Development of Vesper

ReMA’s ISRI Specifications are designed to provide common language in order to facilitate the trading and use of recycled materials (such as aluminum and other metals and materials). The association regularly reviews its specifications to ensure they meet the evolving demands of the global recycling industry, and any company or organization can propose additions, modifications, or deletions.

The ReMA Nonferrous Division initiated the request to create a new specification based on wrought aluminum alloys. Members of the division had noticed that a new type of aluminum scrap was being further processed and consumed in the market place. This new type of aluminum scrap was thanks to the development of multiple advanced sorting technologies, including x-ray fluorescence (XRF), x-ray transmission (XRT), laser-induced breakdown spectroscopy (LIBS), and optical sortation with artificial intelligence (AI).

“These technologies have been in development for many years,” explained Gallo. “More recently, the technology has improved to the point where it can be applied cost-effectively and on a large scale. Beginning in early 2020, Novelis began actively engaging with technology providers, like Sortera, Steinert, and Tomra, to create segregation technologies capable of separating cast and wrought fractions.

Later, this list of technology providers has expanded to include Binder and SGM. In the subsequent years, Novelis has conducted extensive trials with all recycling and technology providers to validate the ability of various technologies to create a vesper specification.”

Development of the vesper specification was officially initiated in 2024, with ReMA staff guiding the process, while the members contributed the research and voted on the final language. “The entire process from initiation to final acceptance into the ReMA Specifications was six months,” said Emily Sanchez, chief economist at ReMA. “The steps involved include the formation of a committee within the Nonferrous Division to look into the proposed creation of a new specification. Then, the group reached out to a broader community of traders and consumers, followed by the full Nonferrous Division for approval. A 20-day public notice was posted and released. Following this public review, the ReMA Board of Directors approved the new specification. Then it went to another public review period of 30 days. With no material comments received, vesper officially became a specification.”

Impact on the Industry

The introduction of the vesper specification will directly benefit the aluminum recycling and casting sector, providing a key definition for trading this grade of scrap material. This is expected to have a number of benefits for the industry. “Recyclers, technology providers, cast, sheet, and extrusion producers will all be able to participate in this new market,” said Landa. “Additionally, consumers of aluminum, like automakers, beverage can producers, and construction product manufacturers will benefit from increased levels of EOL content and the carbon reduction this brings. Recyclers will also benefit from new domestic markets for vesper, which will provide viable options for a scrap stream that has been largely exported as zorba and twitch.”

Vesper could also have an impact on manufacturing for recyclers, casthouses, and consumers, as they adapt to the increased introduction of vesper into the supply chain. Gallo noted some of these potential changes as follows: Customers, like automakers, may need to modify their existing specifications to allow for EOL scrap inclusion. Producers of secondary aluminum ingot (like A-380) will likely see changes to their scrap composition, as the wrought fractions in vesper are recycled by wrought producers. Wrought producers will need to modify processes and specifications to consume this new scrap stream. Scrap recyclers will need to invest in new technology to produce vesper.

“For recyclers, who already produce twitch, producing vesper will likely involve an additional piece of equipment, typically an XRF, XRT, LIBS, or AI device,” explained Gallo. “For producers of zorba, several extra pieces of equipment will likely be required to remove heavier metals (copper, brass, and stainless steel) from aluminum, followed by segregating cast and wrought aluminum to make vesper. As a spec, vesper does not outline analytical limitations other than for iron, but focuses on the compositional limits for things like magnesium and zinc. Typically, aluminum consumers will create their own specifications connected to their purchase orders that specify chemistry requirements.”

Sanchez believes the recycling industry will have no trouble adopting the vesper specification. “Since this material is currently being traded, the industry already acknowledges vesper as a specification,” she said. “ReMA’s ISRI Specifications are reflective of current market conditions and trading practices; they are not aspirational.”

Landa noted that some level of education may be necessary to make the wider market aware of the vesper specification. “Market predictions for vesper generation in North America are significant—the potential is for several hundred thousand tonnes per year,” she explained. “However, vesper production will largely depend on its adoption by aluminum producers and recyclers. Novelis is actively engaged with the Aluminum Association to educate the broader aluminum industry to the emergence of vesper and encourage other aluminum mills to consume vesper and support its market adoption.”

Can you go through a day without hearing the word “datacenter” or “new industrial opportunity / facility?” And then, shortly thereafter you hear about future power needs. A few years ago, we heard how EV’s were going to drive electrification needs. Now it is AI, technology, and the re-industrialization of America.

And remember, we’ve also been told for a number of years about the need for grid modernization. There is / was not enough capacity plus the capacity we have is old and reportedly decaying.

Plus, it is dangerous. Look at the wildfires that occur in the western part of the country. Some by lighting but some by sparks from utilities. And then the need to bury lines.

The investment demand will be massive … and some manufacturers (transformers??) are already in multi-year backlogs.

The opportunity is here (reportedly hyperscalers are “bringing cash to utilities to stimulate support and accelerate development).

NAED commissioned Ducker Carlisle to develop a report for the membership. In the following article, Keith Sarb synopsizes the findings.

Distributors! Take Advantage of the Electrification Opportunity!

Has there been a more exciting time in the electrical industry since the days of Thomas Edison and Nikola Tesla? Demand for electricity in the US is surging, driven by industrial reshoring and the explosion of data centers. This creates opportunities for distributors to capitalize and create new value, but they must move quickly or risk falling behind.

Ducker Carlisle and NAED recently partnered on an in-depth evaluation of electrification trends, growth opportunities, and how distributors can position for advantage (NAED Electrification Research). Two key findings from the evaluation:

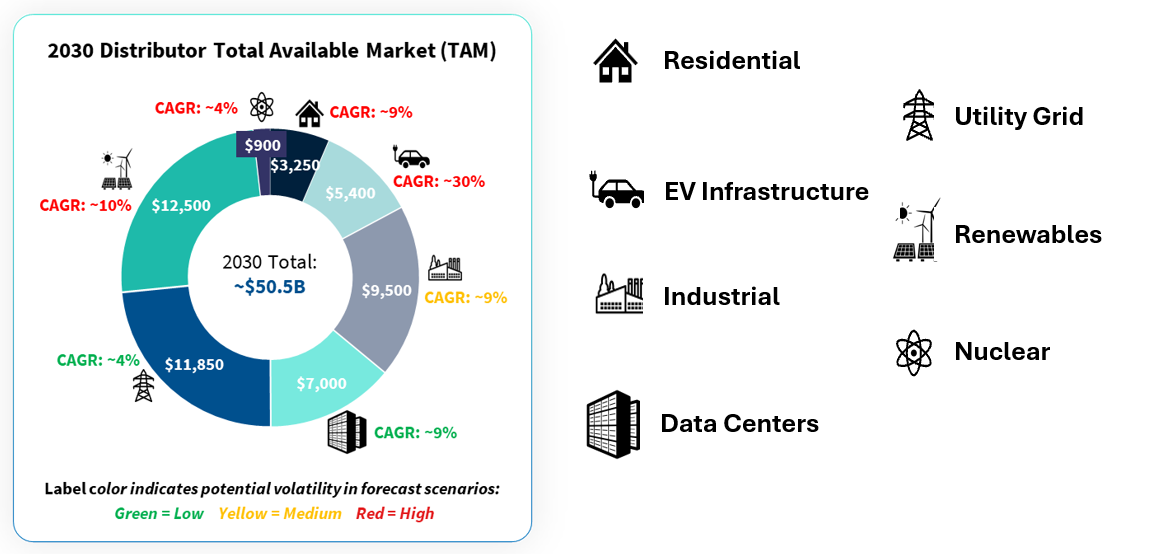

Electrification represents a $50B+ incremental revenue opportunity for distributors by 2030.

Electrification Market Size for Distributors by Segment

The strongest sectors for distributors include Utility Transmission & Distribution, Data Centers, Industrial Facilities, and Utility-Scale Renewables (see Figure 1). In short, the transition to a more electrified economy isn’t a future event, it’s already reshaping where value is created and who captures it.

A Changing Role for Distributors

In these high-growth sectors, projects are becoming increasingly complex and technical, raising expectations of distributors and expanding their role in the value chain. With growing demand, supply chain challenges, and labor shortages, distributors are now being looked to as critical partners in project delivery and productivity improvement.

At the same time, labor productivity in US construction has been flat or declining for decades (see Figure 2), while electrical distributors have achieved significant productivity gains. This creates a clear opening for distributors to lead on efficiency and execution, not simply supply.

Ask yourself:

How can we eliminate bottlenecks in project delivery?

How can we share our productivity expertise with customers?

How can we position as a strategic partner, not just a materials provider?

Distributors that answer these questions early will define the next decade of growth in electrification.

Figure 2: Labor productivity declining in construction and manufacturing, though growing for electrical distributors

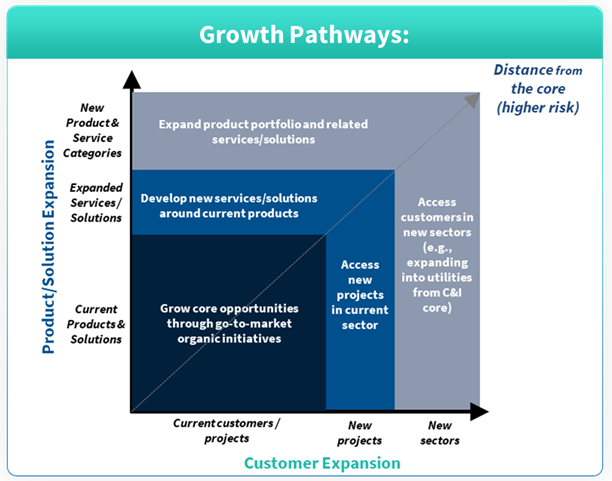

Three Pathways to Create Value