Without surprise, Germany, along with Italy, Poland, and Bulgaria’s support, vetoed the ban on internal combustion engines. This reopens the debate on selecting the appropriate technology for achieving carbon neutrality. However, the discussions will be easier now, without the perspective of having to unravel future regulations. It is becoming urgent for Europe to secure its industry’s future through a technology agnostic approach. Many countries have rushed to force consumers to buy electric vehicles without any consultation or conversion plan to create a supply chain in Europe. Germany’s decision to veto the ban came as rumors were circulating about potential decisions to shift the deadlines (i.e., pushing the ban from 2035 to 2040). In the meantime, the European Efficiency Directive was already stating that most energy related decisions were to be reviewed in February 2024, which means any current enactment would have had a limited duration if elements considered would be discussed less than a year later.

As a result of the veto, decisions made will leave the door open to internal combustion engine vehicles if they run entirely on carbon-neutral fuels. A ban on combustion engines in Europe would focus the industry on electric powertrain technologies to the detriment of R&D efforts towards other carbon-neutral technologies. This would ultimately confine European manufacturers to the EV market, although most European OEMs also serve markets such as Latin America and South-East Asia where electrification is not a priority in terms of mobility solutions.

Europe’s all-electric endeavor was a risky decision given the infrastructure, energy costs, and perspectives of material availability to supply a market of 16 million new vehicles annually that was supposed to ramp up on a 12-year period (2023 to 2035). Such a move would have likely shrunk the European market annual production volume or led to it being predominantly supplied by vehicles from China or North America. European governments have not yet shown a strong support to a European vertically integrated and domestic industry base to fulfill the local demand. Nor has it yet put tariff barriers to limit imports from productions coming from other regions of the world. On the opposite side, the US and the Inflation Reduction Act has led major OEMs to commit to investing in more production in North America, with enough potential to export to Europe. As a result, manufacturers are encouraged by Washington DC to produce electric vehicles locally and at the lowest possible cost, making them affordable to American consumers within a few years.

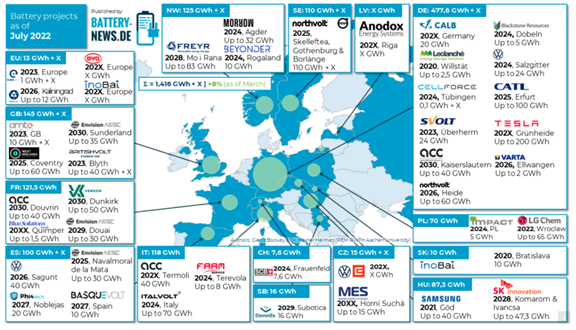

The combustion vehicles ban would inevitably impact production volumes due to materials and vehicles costs, leading to an additional increase in vehicle prices, and making them less affordable for European households. Establishing a new value chain to get better control on costs would take more than ten years. In terms of industrial investment, Europe’s unsteady, inconsistent, and stringent fiscal policy has made the market quite unattractive for several OEMs. Some like GM have left. The 35 factories planned for battery manufacturing also demonstrate a lack of consolidation, and the shyness of each investment, making it a fragmented production base.

Ultimately, the continuously evolving technology and the absence of dialogue with industry leaders are raising doubts about Europe’s capability to achieve their ambitious goals. Europe can look to repetitive failures (in 1996, 2001, and 2008) of the California Air Resources Board (CARB) that enacted unreachable targets then abandoned electrification altogether when reality showed the difficulty to achieve the targets, mostly for energy, financial, and technology reasons. Therefore, while it is important to be ambitious, it is equally important to be realistic to avoid failure.

The European situation is becoming more challenging due to targets causing doubt among industry, energy companies, and citizens. Decisions made by the European Commission and Parliament have driven a certain level of industrial fatigue, illustrated by manufacturers’ departure, and reduced investment in production capacities. This is a significant problem for Germany, a world leader in machinery and production tools. Germany’s choice is aimed at guaranteeing industrial jobs and ensuring access to automobiles for European citizens. Italy’s support to Germany is more of a political stance, while Poland and Bulgaria’s backing of Germany’s decision is based on their strong industrial partnership with the European leader.

European regulators now have the opportunity to take a more cautious approach to carbon neutrality goals and consider a multi-energy strategy. The recent decision by Germany to take a step back is important to avoid losing credibility with global industry participants and investors.

At a turning point for many transformations, it is crucial to ask the right questions, and consider diversification in multiple solutions, sometimes beyond vehicle technology itself. The Japanese example is interesting as the country reduces the environmental impact of vehicles with an extensive development of its infrastructures to limit the daily needs of cars for commuting. If we could achieve automotive pollution control solely through adopting a single lithium-based technology, there would likely be a general craze for a solution that has long been obvious, and the best compromise would already be here.

Governments are necessary to enact, enable, and challenge the implementation of ambitious goals within the range of what technology and industries are capable of. But there are high industrial, social, and economic risks to steer regulations beyond technologies’ capabilities, a path that Germany avoided with its veto.

Article Prepared By:

Bertrand Rakoto, Senior Engagement Manager – Global Automotive Practice Leader at Ducker Carlisle

Leonard Ling, Senior Analyst – Automotive Knowledge Manager at Ducker Carlisle