Why Concrete Contractors Are Positioned For The Next Upcycle

01. 12. 26The U.S. construction industry is nearing the trough of its current cycle, with early indicators pointing to a gradual rebound beginning in 2026, particularly in nonresidential and infrastructure segments that are concrete-intensive. Ducker Carlisle forecasts that total put-in-place construction will rise by 5.3 percent and grow at an average annual rate of 5.7 percent through 2029. However, consensus forecasts from organizations such as the American Institute of Architects (AIA) and the National Association of Home Builders (NAHB) project more moderate growth of 1–3 percent.

These conservative expectations reflect a challenging macroeconomic environment characterized by elevated long-term interest rates, declining consumer confidence, rising tariffs, and persistent labor shortages. Nonetheless, recent actions by the Federal Reserve and expectations of further rate cuts have renewed optimism among market participants that improved funding conditions will stimulate broader construction activity in the coming years.

Residential Construction

Following two years of higher borrowing costs and subdued demand, the U.S. residential construction market is stabilizing after a prolonged downturn. Our outlook indicates that the sector is positioning itself for measured growth through 2029, even as regional trends remain uneven.

As interest rates begin to ease, the housing market is expected to stabilize in 2025 and rebound into 2026 as builders work through existing backlogs and prepare for additional rate cuts to spur single-family home starts. The majority of new housing activity remains concentrated in the South, suggesting that concrete contractors serving these markets can expect rising demand for concrete materials, slab foundations, and masonry block or brick installations.

For concrete contractors, this points to improving bid volumes tied to foundations, flatwork, and masonry in high-growth Southern markets.

Concrete Solutions & the Data Center Expansion

Among the most dynamic areas of construction is the surge in data center development. These projects have become one of the fastest-growing drivers of nonresidential construction, as well-capitalized technology and cloud-service companies continue to invest heavily in expanding capacity. This momentum is driven by ongoing demand for cloud storage, video streaming, and, increasingly, artificial intelligence (AI) and data analytics infrastructure.

We estimate that data center construction will surpass $50 billion by 2029. While large-scale greenfield projects dominate industry headlines, there is also a growing trend toward retrofitting and repurposing existing facilities, particularly those located near established power and energy grids. This trend creates substantial opportunities for concrete contractors, as these facilities require extensive structural reinforcement, poured foundations, tilt-up wall systems, and enhanced energy and water management infrastructure.

For concrete contractors, data centers represent higher-spec work with stricter tolerances, heavier reinforcement, and longer project timelines, rewarding firms that can execute consistently at scale.

Additionally, ancillary developments such as office and high-occupancy support facilities are expected to benefit from this expansion. In contrast, traditional commercial office construction remains constrained by soft occupancy and declining rental rates. Notably, data centers are expected to be a significant source of future electricity demand, with consumption projected to more than double by 2028.

Manufacturing Renaissance

Although manufacturing construction typically moderates following a period of strong expansion, recent shifts in U.S. trade and industrial policy over the past several years are driving renewed domestic investment. Tariff adjustments and incentive programs have encouraged global corporations and sovereign wealth funds to commit significant capital toward U.S. manufacturing projects. This influx of investment is expected to sustain medium-term growth in construction activity, technological innovation, and facility modernization across the sector.

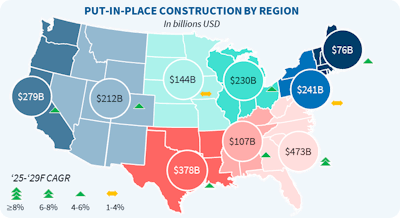

Regional Dynamics

The Southern United States is projected to continue outperforming other regions, accounting for nearly half of total national construction spending by 2029. This sustained growth is supported by structural trends such as net inbound migration, relatively affordable housing markets, and ongoing post-disaster reconstruction efforts.

High-growth states include Texas, Georgia, Arizona, Utah, the Carolinas, and Colorado. Within these regions, suburban and rural markets, particularly Tier-2 and Tier-3 cities are expected to capture outsized development as builders seek lower-cost land and streamlined permitting environments.

These regions are also among the most concrete-intensive markets, driven by population growth, logistics facilities, manufacturing plants, and infrastructure rebuilds.

Emerging Trends for Concrete Contractors

Despite favorable demand conditions, evolving industry dynamics present new opportunities for concrete contractors to enhance competitiveness and long-term performance:

Consolidation: Ongoing challenges related to succession planning, workforce shortages, and geographic diversification are accelerating consolidation among contractors. Strategic mergers and acquisitions, often supported by private equity or outside investors are expected to accelerate through the decade, helping balance market influence between contractors and increasingly consolidated suppliers and distributors.

Distribution Partnerships: While some contractors have recently adopted limited inventory-holding strategies for high-volume products, the variability of project requirements and specialty materials continues to favor strong distributor partnerships. Collaborative relationships with distributors can improve supply-chain efficiency and reduce working-capital strain, ensuring contractors maintain flexibility while mitigating risk.

Source URL : https://www.forconstructionpros.com/concrete/equipment-products/technology-services/article/22957850/ducker-carlisle-why-concrete-contractors-are-positioned-for-the-next-upcycle